TL;DR

President Trump has called for a one-year, 10% cap on U.S. credit card interest rates starting Jan. 20, 2026, drawing rare bipartisan praise in Congress and strong opposition from banks and card issuers.

Why This Matters

Credit card debt is at record levels in the United States, and interest rates are near historic highs. According to Federal Reserve data, average credit card rates now exceed 20%, putting heavy pressure on households that carry balances month to month. The New York Federal Reserve has reported that total U.S. credit card balances recently surpassed $1.23 trillion, an all-time high.

In that context, a proposed 10% ceiling on rates for one year could significantly lower borrowing costs for millions of people. Supporters say it would offer relief to families struggling with inflation and mounting bills. Opponents warn it could instead reduce access to credit, especially for higher-risk borrowers, and push some toward more expensive options such as payday lenders.

The debate also highlights a larger policy question: how far the federal government should go in regulating consumer credit markets. Any move to cap rates would intersect with the work of the Consumer Financial Protection Bureau, which has previously reported that card rates have climbed far faster than banks’ own cost of funds. The outcome could shape how Americans borrow, spend and manage debt in the coming years.

Key Facts & Quotes

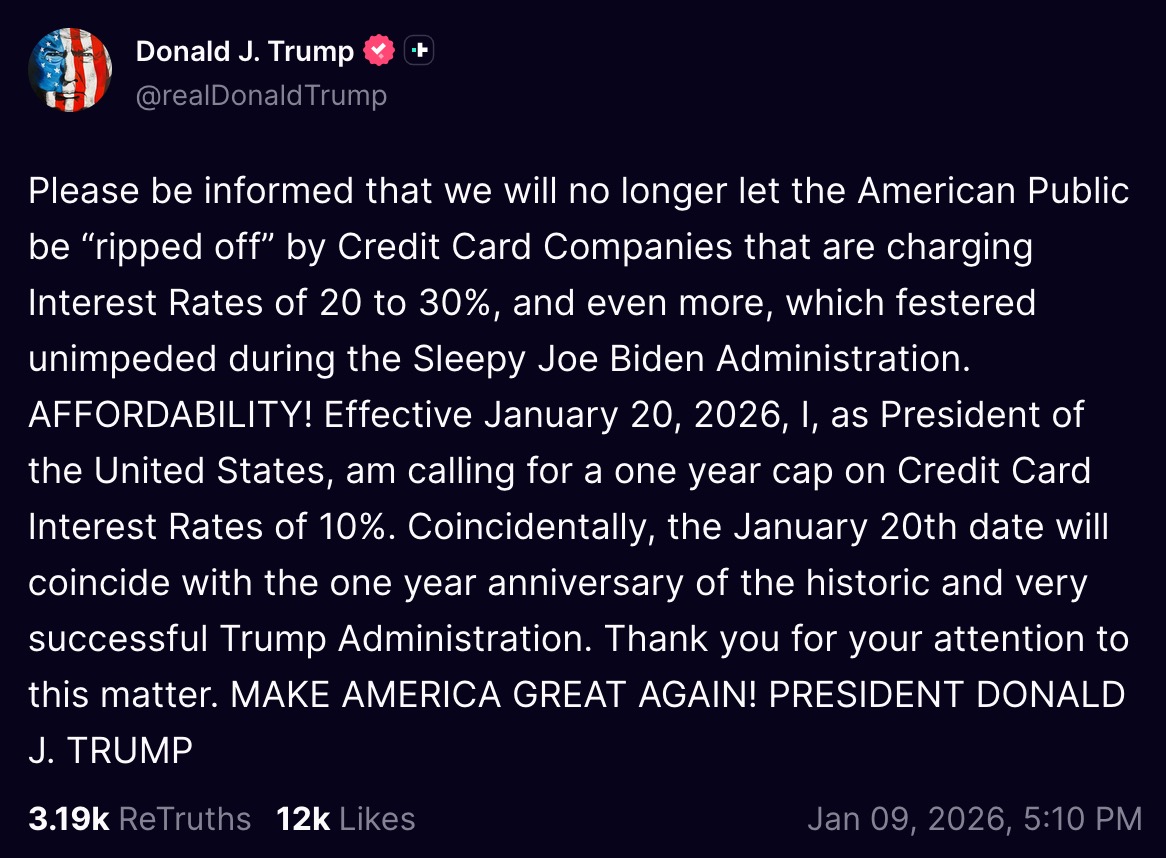

In a late Friday post on Truth Social, President Trump said his administration would “no longer let the American Public be ‘ripped off’ by Credit Card Companies that are charging Interest Rates of 20 to 30%, and even more.” He urged a 10% interest rate cap for one year, starting Jan. 20, 2026, the first anniversary of his second inauguration.

🚨 Trump proposes a 10% credit card rate cap for 1 year

And the downstream effects matter more than people think.A 10% cap could save Americans ~$100B per year in interest payments.

That’s not a theory. That’s cash flow.

US credit card debt sits at $1.21T+

Banks currently… pic.twitter.com/PizIqma1KT

— D Future Money (@DFutureMoney) January 10, 2026

Average credit card rates now top 20%, according to Federal Reserve statistics, so a 10% cap would roughly cut them in half. CBS News reported that the White House has not yet detailed whether the administration will seek to enforce the cap through executive action or rely on pressure to persuade lenders.

The idea has drawn bipartisan interest. Republican Sen. Josh Hawley of Missouri and independent Sen. Bernie Sanders of Vermont introduced legislation last year to impose a 10% ceiling. In the House, Democratic Rep. Alexandria Ocasio-Cortez of New York and Republican Rep. Anna Paulina Luna of Florida backed a similar measure. “We cannot continue to allow big banks to make huge profits ripping off the American people,” Sanders said in a prior joint statement with Hawley.

Industry groups strongly disagree. The American Bankers Association, the Bank Policy Institute and the Electronic Payments Coalition warned that a one-size-fits-all 10% cap would reduce credit availability and could be “devastating” for families and small businesses that rely on cards. Billionaire investor Bill Ackman, who supported Trump’s 2024 campaign, called the idea a “mistake,” arguing on X that lenders would cancel cards for millions of consumers if they cannot cover losses and earn returns.

Scott Simpson, CEO of America’s Credit Unions, said in a statement to CBS News that while the goal of affordability is understandable, “capping rates at 10% does not make credit more affordable, it makes it unattainable for millions of working Americans.”

What It Means for You

If a 10% cap were implemented and fully applied, Americans who carry balances could see sharply lower interest costs for at least a year. That could make it easier to pay down debt, especially for households already stretched by housing, food and medical expenses. For older adults helping children or parents with bills, lower card rates could ease some financial strain.

However, banks and card issuers say they may respond by tightening credit standards, cutting limits, reducing rewards or closing some accounts. That could make it harder for people with weaker credit scores to qualify for cards at all. Consumers might then turn to alternatives like payday lenders or pawn shops, which often charge much higher rates.

For now, nothing has changed on existing cards. The next steps to watch are whether the White House moves to issue an order, whether Congress revisits rate-cap legislation, and how regulators such as the Federal Reserve and the Consumer Financial Protection Bureau react.

Sources: CBS News report published Jan. 20, 2026; Federal Reserve and Federal Reserve Bank of New York consumer credit data; prior Consumer Financial Protection Bureau research on credit card pricing; statements by lawmakers, industry groups and investors cited in official releases and public posts.

Do you think a temporary 10% cap on credit card interest would help more Americans than it might hurt, or are you more concerned about reduced access to credit?